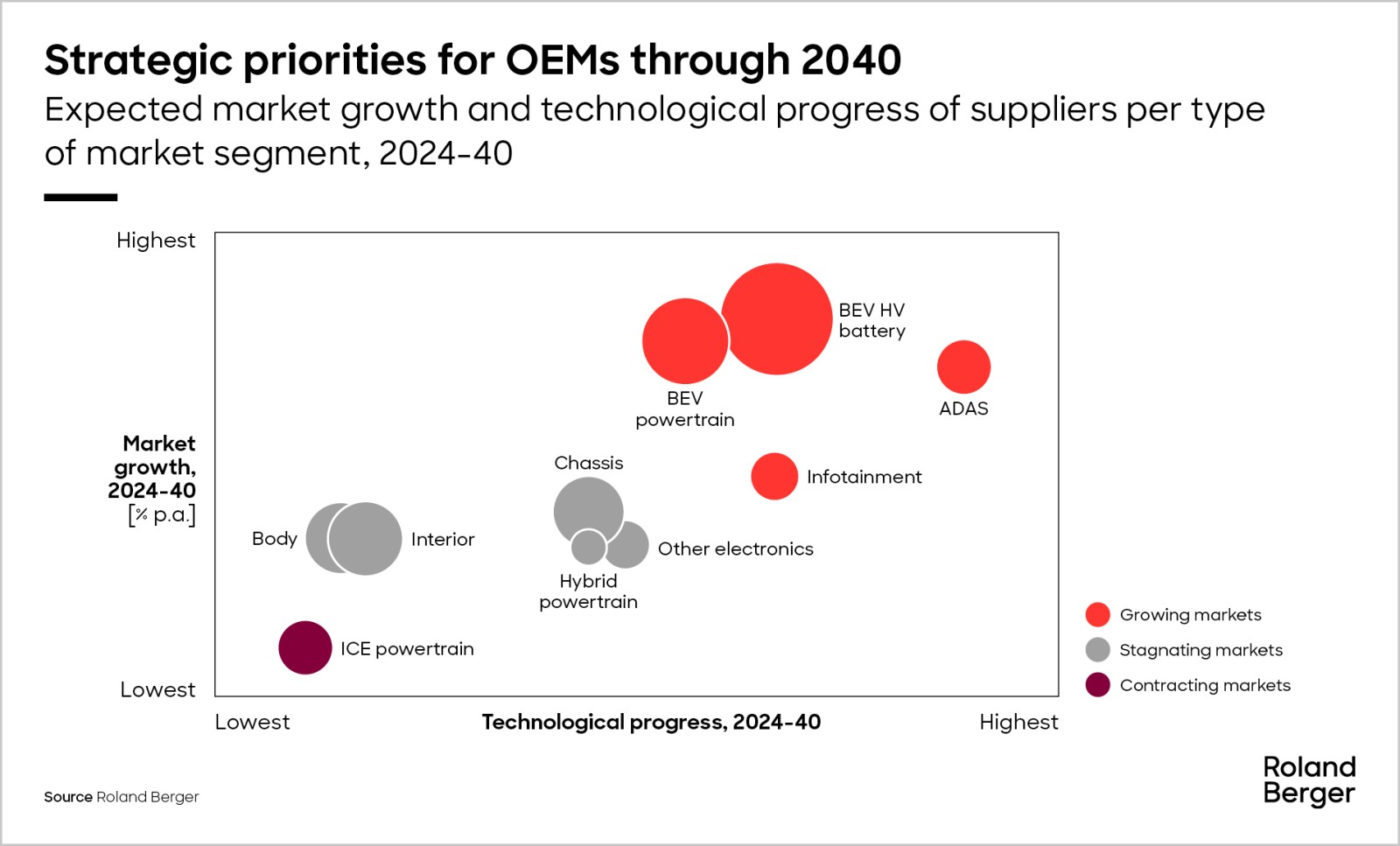

Consolidation ahead

The next decade and a half will bring a number of changes directly affecting suppliers. First, suppliers will benefit from new sourcing behavior by OEMs. Many OEMs will increase their insourcing in the short term to leverage technology-driven differentiation, especially in fast-growing domains such as BEV HV batteries, the BEV powertrain and E/E systems. However, we expect this trend to peak before the end of the current decade as technological maturity increases, after which many may choose to rely once again on scale, standardization and the resulting cost advantages by sourcing through suppliers. This development will give an extra boost to suppliers best positioned to tap into this fresh opportunity.

Second, it is likely that growing system complexity will speed up market consolidation. Today's Tier-1 supplier landscape is fragmented and in the period to 2040 we expect to see a strong acceleration of ongoing consolidation, as scale increasingly becomes the winning factor in a highly competitive market. This will be driven by OEMs' preference for sourcing from a few large system suppliers so as to reduce complexity and costs.

Third, we already see established technology players from other industries entering automotive component domains, investing heavily in building expertise and expanding their market share. In some cases, these new entrants may force existing suppliers out of the market.

Winning strategies

Suppliers therefore need to engage in strategic thinking. Players operating in contracting market segments will need to balance the growing pressure to consolidate with securing sufficient supply for their customers. To some extent this will remain true even beyond 2040, although we believe that only a few suppliers will make it through to 2040 and beyond. Winning strategies potentially include building a regional portfolio accounting for different BEV trajectories, focusing on continuous performance improvement, pursuing partnerships or M&A, and divesting early in areas where success is at risk or initiating a structured wind-up process.

![Component revenue pool by domain and region, 2024 vs. 2040 [EUR bn; % growth p.a.]](/content_assets/content_images/captions/Roland_Berger_24_2032_Auto2040_Supplier_GT02_large_image-2.jpg)