Cementing your position in cement

By Sayak Datta

The Southeast Asia cement industry is at a pivotal point, citing a clear need for players to think and act differently.

"Multiple external factors such as rising coal and electricity prices have compounded the problems for cement players across SEA markets. Passing through the entire cost increase to the consumer is unlikely, leading to margin pressures for many SEA cement players."

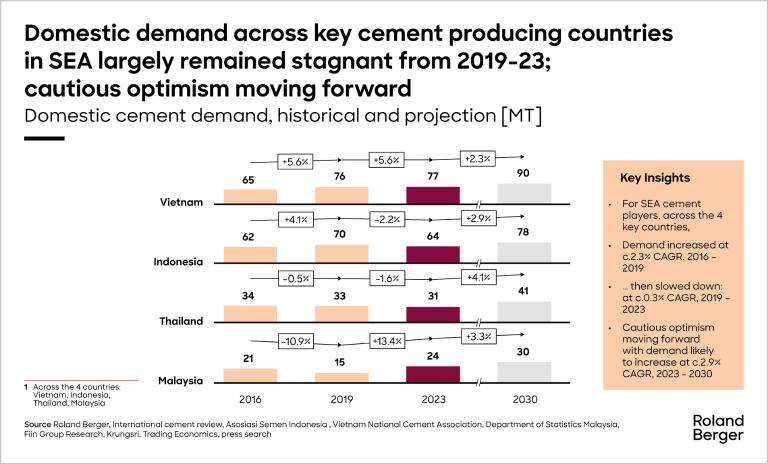

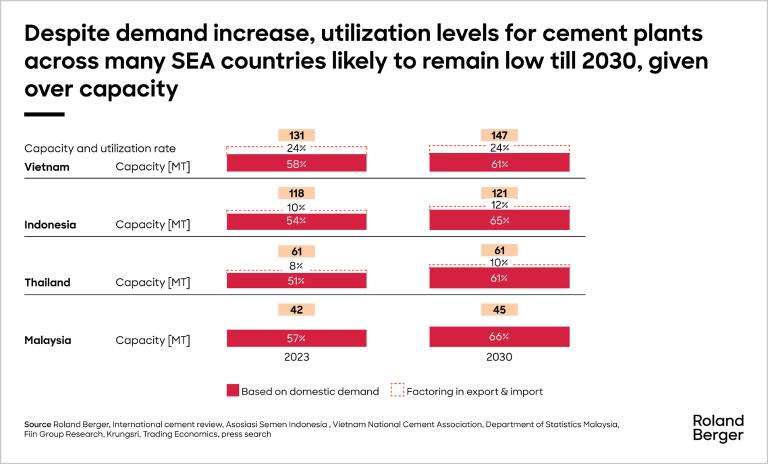

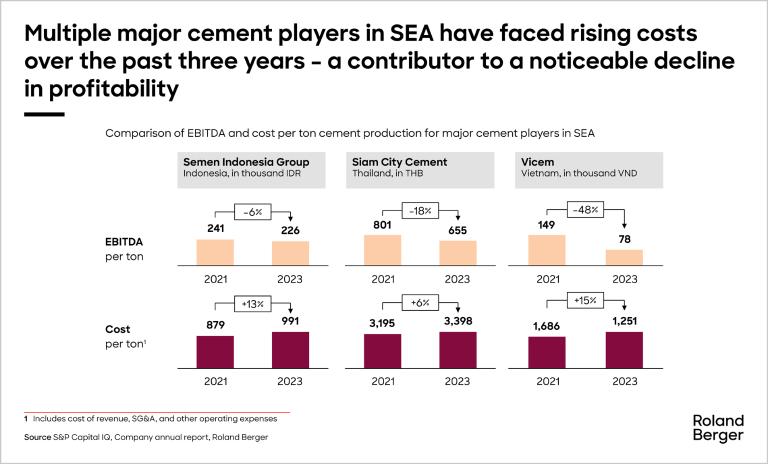

Around 7% of the global cement production is from SEA, signifying the region’s importance in the global landscape. However, cement demand in the region grew at only 0.9% CAGR from 2019-2023, showcasing a stagnating market compared to ~2.3% CAGR from 2016-2019. This has led to a 50%-60% utilization level for cement plants across SEA as of 2023, revealing overcapacity in the market. A deeper look at the financial performance of some of the larger cement players in SEA reveals declining profitability from 2021 to 2023, despite revenue growth in some cases, while many global players performed better over the same timeframe. What are the implications for the industry, and where does it go from here? At Roland Berger, we offer valuable insights into the Southeast Asia cement industry by analyzing current data and trends. Through primary research and extensive industry research, we identify five key trends & five must-win themes that cement players must focus on to succeed.

External pressure on demand

Macro factors such as rising interest rates, post-COVID slowdowns in government spending on large-scale projects, and continuing geopolitical uncertainty have increasingly put pressure on the construction industry.

There are several examples of delayed projects: the Bangkok–Nakhon Ratchasima high-speed railway in Thailand, delayed until 2027, is reportedly currently 36% behind schedule. In Vietnam, slow implementation of public investment projects and a stagnant housing market have added to the woes.

Sustained overcapacity

The cement market is facing an over-capacity in several SEA markets. Reduced domestic demand has also forced many SEA cement players to turn their faces towards export markets.

However, exports can be highly volatile due to multiple factors such as changing geopolitical situations and evolving local markets, and therefore, utilization levels in SEA countries will be largely driven by domestic demand.

Rising input costs

Rising input costs have increased margin pressures for SEA cement players, as it is not likely for them fully pass on costs to end consumers.

A key driver of rising input costs is coal, which typically contributes to approximately 25 – 30% of the total cost of cement production. Increasing electricity tariffs in some countries, like Vietnam, has also posed a problem.

Increasing competition

The competitive landscape for cement in SEA is heating up, especially due to Chinese cement producers. The total production capacity of Chinese cement players in SEA (i.e., in Indonesia and Vietnam) increased to approximately 24 million tons per year in 2023, roughly 10% of the total capacity across these countries and 7% overall for SEA.

Over the years, the SEA cement sector has witnessed several M&A transactions, and given the increased competition, among other factors, we could potentially see more in the next few years.

Increasing pressure on sustainability

There are signals of increasing sustainability pressure on SEA cement players, driven by the countries’ nationally determined contribution (NDC) targets, as well as by investors.

For players looking to export cement, border adjustment tariffs could also pose challenges. Rather than looking at it as a challenge, SEA cement players need to look at this as an opportunity to differentiate and contribute towards national sustainability goals.

Conclusion

Given the trends, the cement industry in SEA has faced increasing financial pressure in recent years. The average Return of Capital (ROC) on a long-term basis, i.e., for the last 20 years, for cement players in SEA averaged at around 6.4%. In contrast, their global counterparts (excluding SEA) have achieved a higher average of around 8.3%.

While the challenges are significant, the opportunities are even greater. SEA cement players must seize the moment—exploring new frontiers for resilience, differentiation, and investor appeal. With this in mind, we have identified five must-win themes that are crucial for SEA cement players.

Register now to access the full study and explore the emerging trends and potential in the SEA cement sector.

Furthermore, you get regular news and updates directly in your inbox.

The next five years will be dynamic for SEA cement players, and it will come down to the choices that players make.