The situation is becoming even more challenging when considering some other factors at play:

- High costs: Europe is currently at the end of the cost curve in many value chains due to high energy and raw material prices, and an old asset base.

- Fierce competition: Competition from the US, China and the Middle East is increasing, thereby challenging Europe's footprint.

- Strict regulations and lack of incentives: Europe sets strict regulatory frameworks for the transition, but lacks strong and transparent incentive programs. Other regions meanwhile are pursuing fervent investment agendas within their own borders.

- Unfavorable sentiment: Europe has a challenging public and regulatory environment for industrial investment and activities, although the tide is turning (e.g., through the Antwerp Declaration and increasing political recognition of the urgent situation).

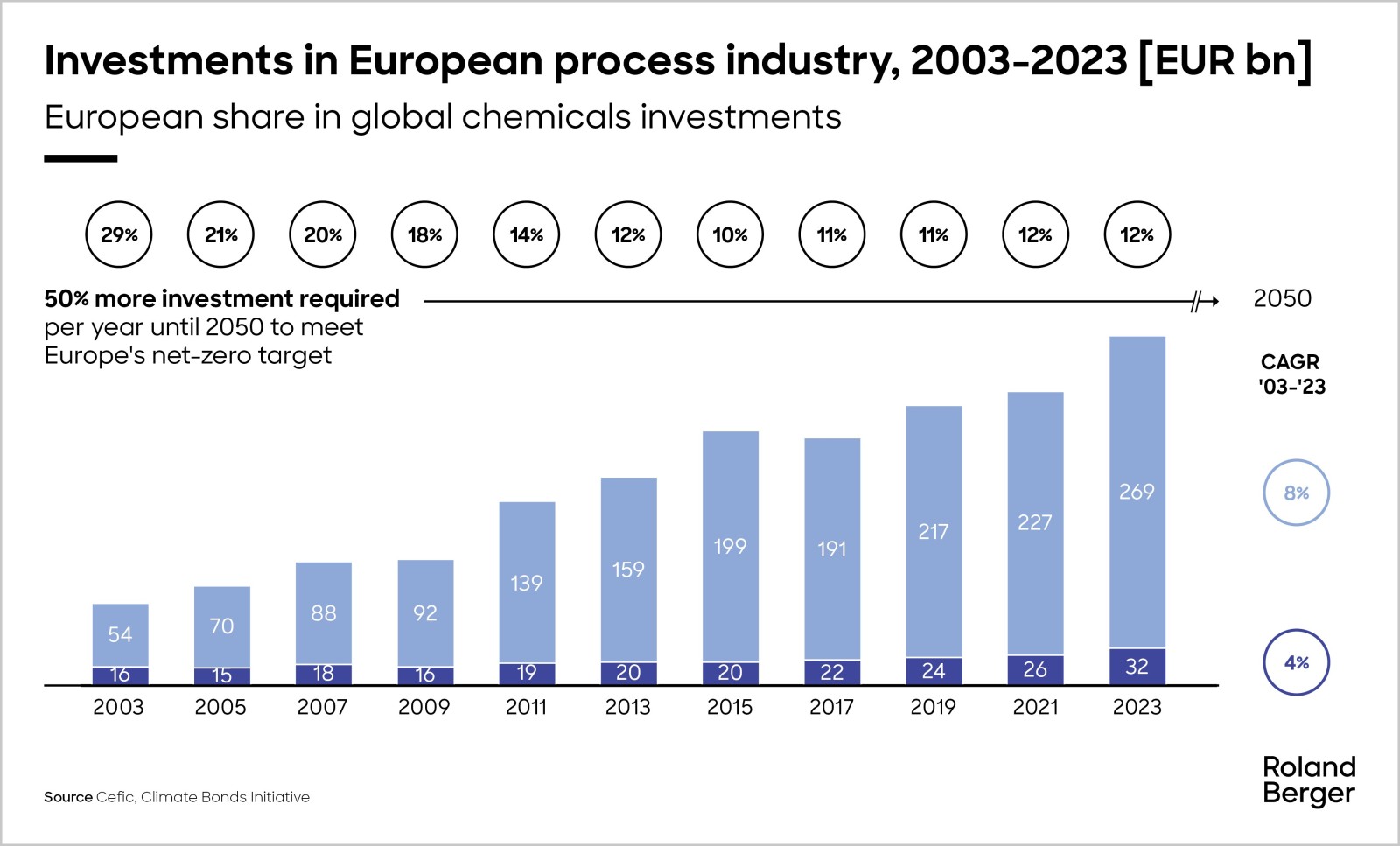

As a result, many projects in Europe have been canceled or postponed. There are too many risks in the system, pushing chemicals players to prioritize investments elsewhere.

Opportunities for Europe

But this does not mean that there are no opportunities in Europe. When looking from a value chain perspective, we see risks, but also opportunities in resilient value chains, value chains that will be disrupted or even broken up, and value chains that will emerge, driven by strategic autonomy.

Resilient value chains are those where Europe has traditionally had a strong position due to strong local end-markets, local feedstocks, integration in local chemical sites and value chains, or a combination of these and other factors. Though utilization is down in many of this type of value chain, they are expected to stay relevant precisely because of the factors that ensured their strong competitive position in the first place.

Disrupted value chains are expected to undergo significant change because of the transition to more circular and decarbonized feedstocks and production processes.

Due to diminished cost-competitiveness along some part of the chain, there are also some value chains that are expected to be broken up. In these chains, we will see that some steps in the value chain will be moved to other regions, of which the product will be imported and processed further in Europe.

Lastly, some value chains are expected to emerge or grow driven by strategic autonomy demands. Supply shortages following COVID-19 and geopolitical events have exposed Europe’s dependence on foreign production and manufacturing in key areas.

Recommendations

Policy makers will have a role to play, and chemical companies can take action to position themselves to capture the opportunities in Europe. To help European chemical companies make these plays, we have identified six crucial steps, as well as steps policymakers need to take to support and protect the sustainable transition of the European industry.

Do you want to gain a better understanding of the challenges and opportunities in the European industries from a value chain perspective? Do you want to learn the six crucial steps we have identified that can help European players to futureproof their value chains? Download the full study and reach out to discuss how we can help you prepare for the transition ahead.

We invite you to stay tuned for part 2, "The ecological-economic balancing act", where we will examine the intricate geopolitical and macroeconomic dynamics currently challenging Europe’s chemicals industry. We will delve into the disruptions faced by companies, the shifting investment landscape, and the essential adaptations required for the industry to navigate its path towards sustainability while balancing economic viability.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland-Berger_Navigating-European-Chemicals_cover_DEF_download_preview.jpg)

_person_320.png?v=1687234)

_person_320.png?v=1687234)