Electric mobility is creating economic opportunity and decarbonising a top-emitting sector

The transformation to electrified road transport is well underway. Like solar and wind before it, the expanding UK eMobility sector is creating significant economic opportunities as the nation decarbonises one of its most emitting sectors.

The diverse range of companies driving this forward are increasing productivity and investing across the UK – from automotive manufacturers to innovative electric vehicle (EV) lessors and electric commercial vehicle as a service providers – showing the sector’s adaptability to meet evolving transportation needs.

Meanwhile, substantial investment in EV charging infrastructure is transforming the user experience, making EV charging more available and more convenient than ever before. And as the UK invests billions into renewable energy, the role of eMobility in greening the grid cannot be overstated. The sector is critical to the UK’s energy transition.

Considerable success has already been achieved, and commitments to growth are there from key players. However, current momentum and confidence in EVs must be maintained to fully realise the significant economic potential.

"The investment of billions of pounds into UK eMobility is already paying off for example with major improvements in public charging provision and user experience."

The UK eMobility landscape is large, diverse, and growing fast

This dynamic sector is evolving rapidly, driven by significant investments into people, infrastructure and intellectual property from players old and new.

Long-standing incumbents within the automotive manufacturing sector are pivoting their operations to electric. Notably, automotive OEMs have collectively committed over £11 billion to building new models and components. This strategic shift is projected to create or secure jobs for more than 16,000 people, as indicated in their public statements.

In addition to the shifts among established players, new sectors catering specifically to electric road transport are growing fast. These already employ thousands of people and are establishing essential infrastructure and critical, exportable intellectual property.

Charge Point Operators (CPOs) have invested over £1.5 billion to date in the installation and maintenance of public and commercial vehicle charging infrastructure, with an anticipated further investment of over £8 billion by 2030 to enhance these networks.

The broader EV charging industry, encompassing CPOs and charge point installation and maintenance services, currently employs over 4,000 individuals. This number is expected to exceed 10,000 by 2030.

Emerging leaders in the sector are attracting substantial outside investment: CPOs collectively raised £2 billion; British bus and truck electrification end-to-end solutions provider Zenobe £1.8 billion; and electric-only leasing provider Octopus Electric Vehicles £650 million.

Furthermore, a plethora of UK-based eMobility service providers (eMSPs) are developing critical intellectual property in areas such as charge point management and smart charging, which create high-value job opportunities and exportable capabilities.

All these developments drive the UK closer to a decarbonized transport sector and a greener grid. Substantial progress has been made toward these objectives, and it is crucial that momentum and investor confidence in the sector is maintained; now is not the time to ease off on these efforts.

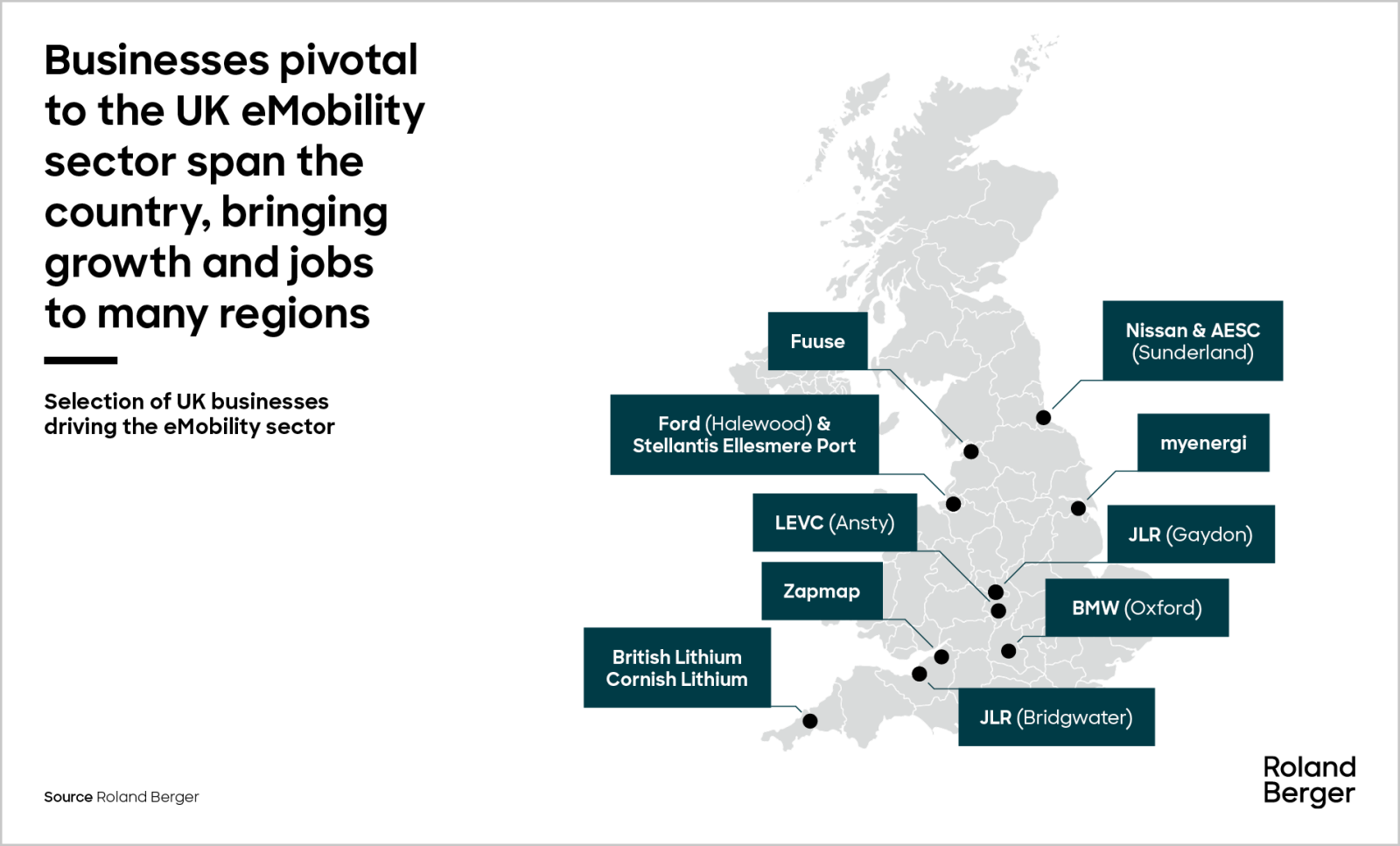

The economic benefits of a diverse sector span the nation

Building a UK-wide network of charging infrastructure naturally creates regional jobs in charge point installation, and long-term regional productivity in the service and maintenance of the network. Head offices, factories and warehouses of eMobility businesses span the nation, for example charge point manufacturer myenergi in the Humber and prominent eMSP Zapmap in Bristol. The emerging Cornish and British Lithium industries are creating opportunities in Cornwall.

The biggest regional employers of the sector, however, are the automotive OEMs. Many of these have made substantial public commitments to investment and job creation or security at plants from Sunderland to Bridgwater (see map).

Geely factory at Ansty (£500 million, 1000 jobs)

Nissan Leaf and AESC factory in Sunderland (£420 million)

£3 billion further commitment from Nissan (Sunderland)

£4 billion commitment from JLR (Bridgwater)

£500 million further commitment from JLR (Merseyside)

BMW Oxford and Swindon (£600 million)

£2 billion commitment from Aston Martin

Other commitments include investment from Ford and Stellantis (Merseyside).

Collectively these commitments contribute over £11 billion of investment and over 16,000 jobs to the British economy, based on public announcements by OEMs.

Investment in innovative British business does not stop there. The diverse range of companies driving the sector forward, and creating world-leading products and services, include end-to-end fleet electrification provider Zenobe (which has raised £1.8 bn in inward investment), and EV leasing company Octopus Electric Vehicles (£650 m). These are genuine success stories showcasing the UK’s potential to lead in a dynamic and rapidly growing sector.

Investment into charging infrastructure and falling vehicle prices make now a better time than ever to drive an EV

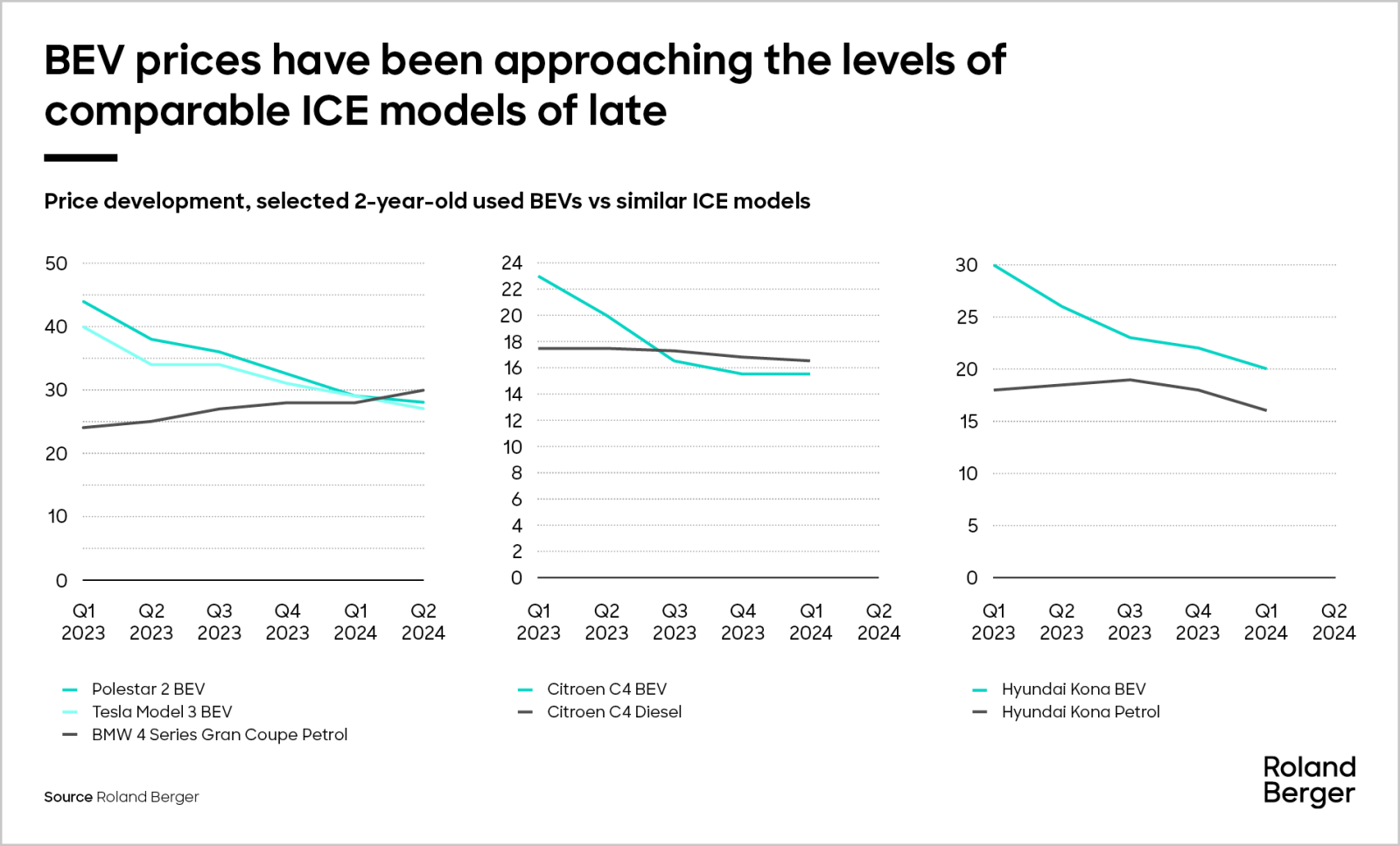

Investment into charging infrastructure is significantly enhancing the experience of owning an EV, particularly as prices converge with those of internal combustion engine (ICE) vehicles.

"eMobility plays a critical role in the UK’s energy transition, driving growth in clean energy and innovation in demand management."

To date, CPOs have invested over £1.5 billion in public and commercial vehicle charging infrastructure. To meet the growing demands for both passenger and commercial vehicle charging by 2030, they will invest at least another £8 billion.

Supporting this ambitious expansion, investors have committed approximately £2 billion in debt and equity funding to charge point operators alone. Notable raises include over £500 million into Gridserve in equity and loan facilities, and more than £250 million into Raw Charging. Such investment is crucial for creating a high-quality charging network and achieving the sector's ambitious targets in the coming years.

Additionally, UK eMSPs are actively bringing solutions to market, leveraging valuable intellectual property that enhances the charging experience and operational efficiency, with notable examples including Zapmap (mapping and payments), Bonnet (route planning and payments), EV.Energy (energy management), and Fuuse and Switch (EV charge point management).

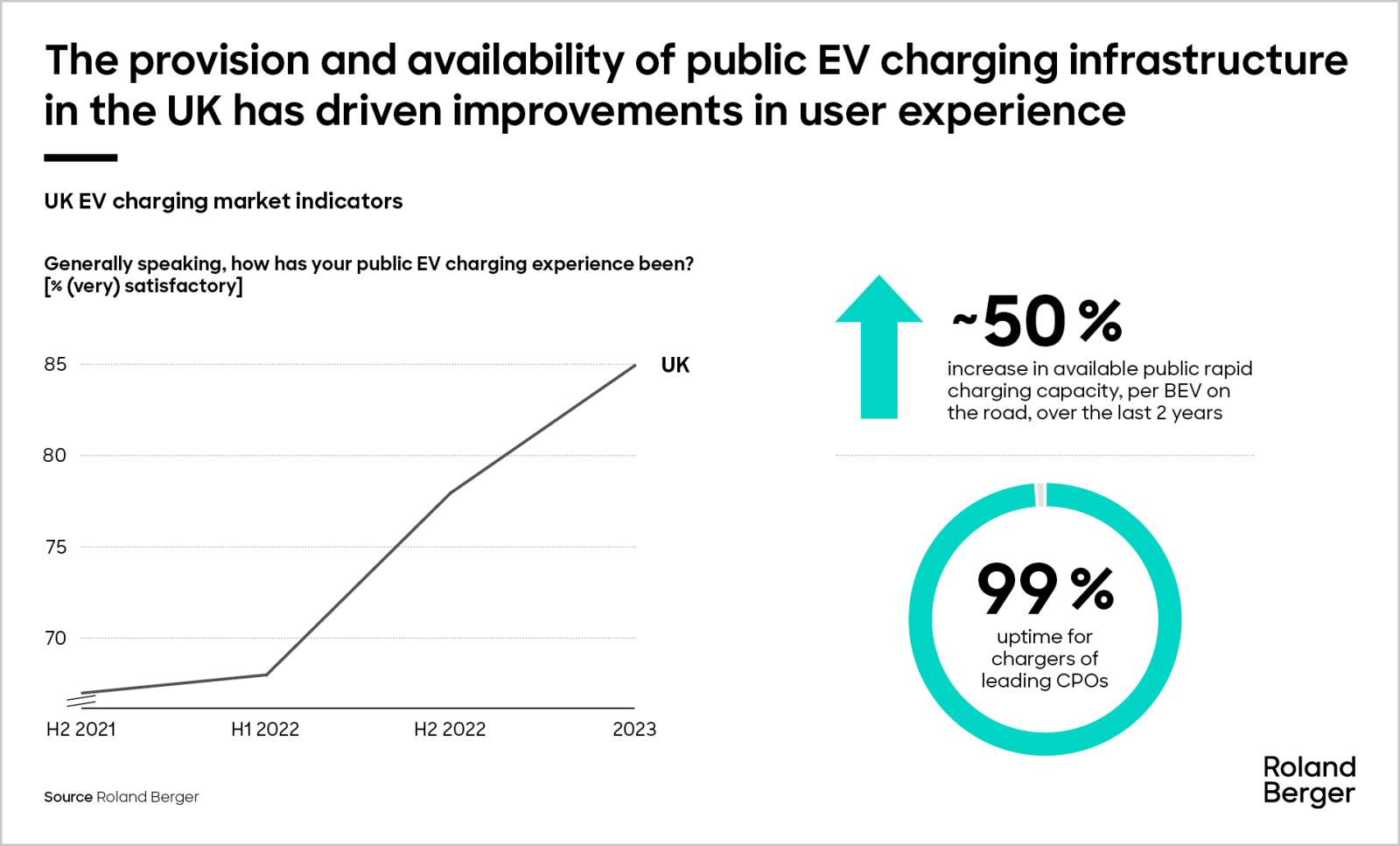

The commitment from the sector is already bearing fruit, with UK drivers reporting some of the highest charging experience satisfaction in Europe, based on Roland Berger’s EV Charging Index and other surveys.

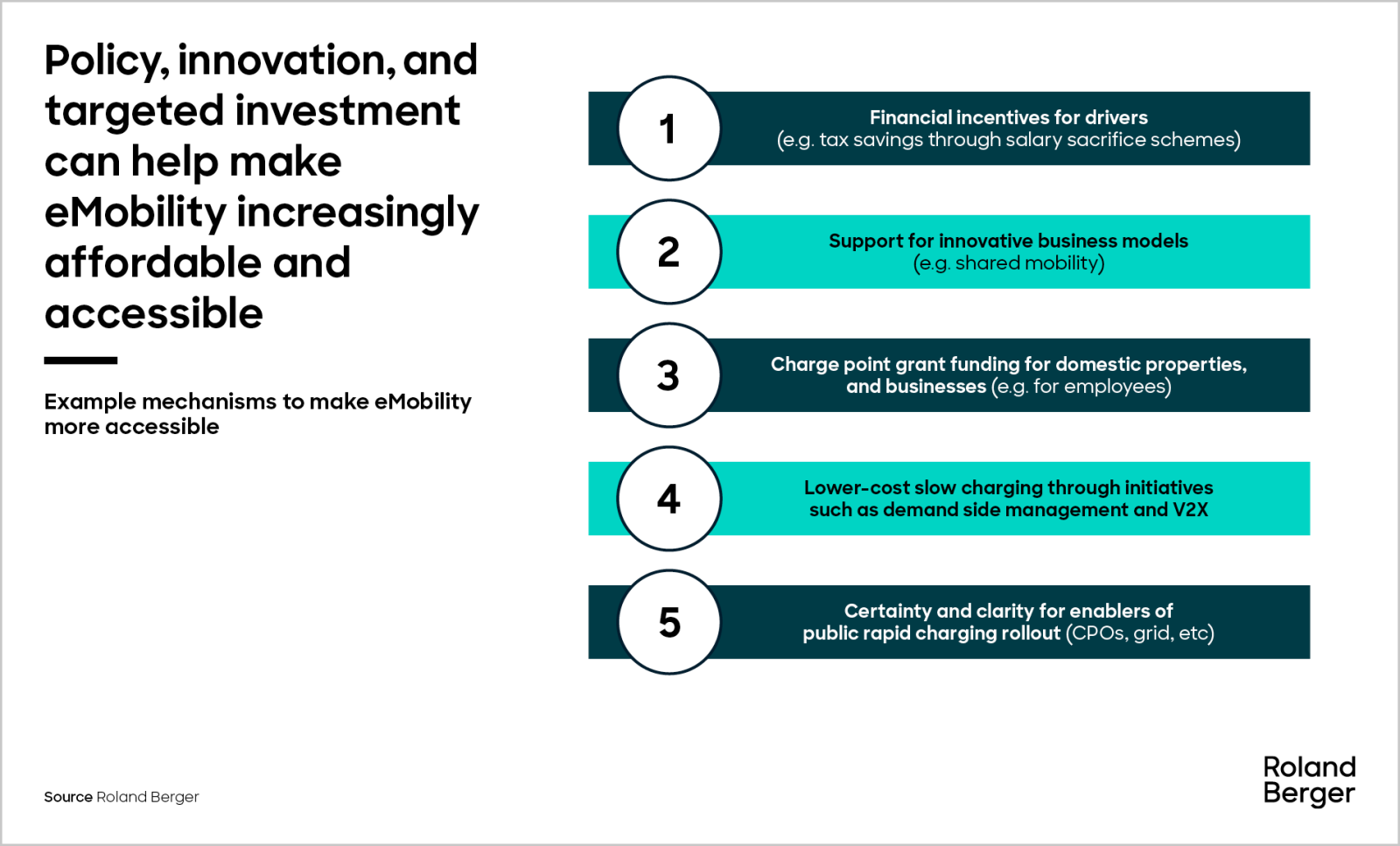

As EV and ICE vehicle prices converge across market segments and vehicle types, various mechanisms are making EV ownership even more economical, from attractive salary sacrifice schemes to a burgeoning second-hand market and charge point grants.

With the removal of key barriers around vehicle costs and charging experience, driving an EV is becoming ever more positive. These investment and innovation trends must continue if the UK is to realise the economic potential of the eMobility sector.

eMobility is at the heart of the UK’s energy transition

The role that eMobility plays in the UK’s energy transition should not be underestimated: it will drive growth in the clean energy sector and innovation in demand management, and ultimately support energy security.

Clean energy demand is expected to increase as both home and public chargers procure renewably. This will drive overall growth to the energy sector but particularly support the development of renewable generation and storage capacity in the UK. As an indication, the current ~35 GW of solar, onshore wind and offshore wind awarded under the UK government’s Contracts for Difference (CfD) scheme will involve over £60 bn of investment to build and install when all completed.

EV batteries themselves are a storage and demand management opportunity, if coupled with technological development and regulation. This in turn supports renewable generation by flattening peak demand, as well as creating software jobs.

Finally, investing in the transition to electric helps de-risk the energy supply chain: reliable UK renewable generation and storage capacity reduces our dependency on imports of foreign oil.

A strong start

This is an area which, despite challenges, has achieved considerable early success and attracted significant, long-term investment.

From automotive manufacturing to charge point operation to consumer app development, the businesses electrifying road transport make up a diverse sector that employs thousands of people across regions and skillsets. Inward investment to date is significant, and already paying off as key indicators around EVs improve dramatically. And there is more to come, with billions of pounds publicly committed and tens of thousands of jobs created and secured.

In the longer term, development of a robust electrified transport system also drives growth, economic benefits and employment opportunities in crucial sectors such as clean energy, energy security and grid infrastructure. It is critical to the UK’s energy transition.

The momentum in the sector is building. Maintaining confidence in the ZEV market and pace of transition will continue to drive growth already underway, and realise the full economic opportunity ahead.

Notes on methodology and sourcing

Figures for inbound or committed investment in a sector include data for the largest companies in that sector where the size of the investment is disclosed – therefore the true figure is likely higher. This excludes the figures for electric vehicle charger installation and maintenance (capex, opex and employment), which were calculated through RB modelling.

Data sources used include ZapMap, MergerMarket, IHS, European Association of Electrical Contractors, SMMT, DfT, Auto Trader, Indicata, Companies House, IRENA and the Department for Energy Security and Net Zero, and Roland Berger’s EV Charging Index.

Download the article

Article

The present and future economic case for eMobility in the UK

The UK’s electric mobility transformation is well underway. Maintaining momentum and confidence in the sector is key to realising its significant economic potential.

_image_caption_none.jpg)